Life Insurance, Stock Market, SCPI: Which Investment for 2026?

Here is the classic dilemma for French savers: what to do with their money when looking ahead to 2026. Between PELs maturing, inflation slowly eroding purchasing power, and yields collapsing everywhere, the question becomes urgent. Life insurance, stock market, or SCPI? Each has its strengths, its weaknesses, and above all, each meets different needs depending on your profile and investment horizon.

Table des matières

Life Insurance: Controllable Stability 🛡️

Life insurance remains the favorite investment of the French. And for good reason: it is the most versatile tax wrapper, one that adapts to all profiles. But beware, it is not a one-size-fits-all formula. It comes in two very different varieties that correspond to diametrically opposed strategies.

Euro funds: zero risk, but patience required

This is the product that reassures above all. Your capital is guaranteed. It cannot decrease. Period. Euro fund yields posted performances around 2.50% to 3.50% in 2024, depending on the contracts. Some top performers like Placement Direct (3.45%) or Mif Horizon Euroactif (3.35%) pulled the ranking upward.

But 2026 will be less cheerful. Inflation is slowing, ECB rates remain steady at 2.00%, and this weighs on euro fund returns. Projections suggest that yields could stagnate around 2.5% to 3.0% in 2026, a level barely above real inflation. This is the price of absolute security.

The big advantage? If you do not touch your money for 8 years, your taxation becomes ultra-favorable: social contributions drop from 17.2% to zero, and income tax is drastically reduced. In other words, it is an investment for the patient who knows they will let their savings lie dormant for a long time.

Unit-linked funds: the growth engine

This is where life insurance becomes truly interesting for those who accept some volatility. Unit-linked funds are your stocks, bonds, ETFs, SCPIs held within the protected envelope of life insurance. You keep the flexibility of the investment, but under the tax umbrella of insurance.

Depending on the mix you choose, returns can vary greatly. A 100% European equity allocation targets 7% to 12% annually, but with high volatility (18 to 25%). A balanced allocation (60% equities, 40% bonds) aims for 4.5% to 6.5% with less turbulence. Bonds alone yield 3% to 5%. The choice really depends on your tolerance for shocks.

The tactical advantage: zero entry fees and zero switching fees with the best contracts like Placement Direct, Linxea Spirit, or Lucya Cardif. Annual management fees hover around 0.5% to 1.0%, which is reasonable. Another major bonus: you can access more than 1,300 different supports in multi-support life insurance. This means you can build an ultra-diversified portfolio without leaving your tax wrapper.

The Stock Market: Potential, But Volatility 📈

Stock markets in 2026, that’s the big debate. Analysts do not all agree, but a trend is emerging: European stock exchanges should continue to progress, notably thanks to the expected drop in ECB rates. Let’s see concretely what experts project.

The CAC 40 outlook for 2026

Analysts’ projections place the CAC 40 around 9,000 to 10,600 points in 2026, compared to 8,100 points today. This would represent an increase of 10% to 30% depending on the scenario. The drivers? Economic growth stabilizing (1.0% in 2026 according to the ECB), inflation converging towards 2% (ECB target for 2026), and European companies expected to see their profits gradually rise.

But beware: it’s not linear. French economists anticipate weaker growth (0.9% for 2026), which slightly cools enthusiasm. Stock returns will also depend on political and geopolitical factors that are unpredictable today. A trade war, an oil shock, a banking crisis… and everything can change.

What returns to expect in 2026?

European stocks historically offer an average return of 7% to 12% annually over the long term. But the short term can be very volatile: you can gain 20% one year and lose 15% the next. The Dividend Yield of the CAC 40 is currently around 3.5% to 4%, which is interesting for regular income.

For tech or American stocks, the appetite for returns remains higher (8% to 15%), but so does volatility (25% to 35% annually). This means that if you seek pure growth, you must accept that your portfolio may plunge 25% some years. Not for the faint-hearted.

The importance of stock market taxation in 2026

This is a key point often forgotten that can really ruin your returns. If you hold stocks directly in a regular securities account, you will pay 19% income tax + 17.2% social contributions = 36.2% total taxation on your capital gains and dividends. It’s horrible.

But if you hold your stocks in a PEA (Equity Savings Plan), taxation becomes almost free after 5 years: zero tax, zero contributions. That’s huge. You can also earn €50,000 on the stock market and pay no tax if it’s through a PEA held for 5+ years. So, for stocks, prefer the PEA over a regular securities account, unless you exceed the limit (€150,000 per person).

SCPI: Real Estate Without Managing 🏢

SCPIs are Civil Real Estate Investment Companies. Concretely, you invest in a fund that holds a portfolio of buildings (offices, shops, housing, warehouses, hotels). You receive your share of the rents collected. It’s very simple, and it’s attractive for all those who dream of real estate income without becoming landlord-owners.

Record yields of 2025-2026

The year 2025 is exceptional for SCPIs. The French Association of SCPIs (ASPIM) forecasts an average market yield around 5.0% in 2025, with about forty SCPIs showing more than 6%, and about ten flirting with 10%. Names like Sofidynamic (9.52%), Transitions Europe (8.25%) or Wemo One far exceed historical expectations.

Why this success? Managers took advantage of the 2022-2023 crisis to buy quality buildings at bargain prices. These cheap purchases now translate into high yields for the partners. It’s good real estate management benefiting patient investors.

For 2026, experts at La Centrale des SCPI expect a stabilization around 4.5% to 6.5% depending on the SCPI. Less spectacular than 2025, but still attractive compared to secure alternatives like bonds.

The Weak Point: Illiquidity and Fees

Here is the downside: SCPI shares are not as liquid as stocks or ETFs. You often have to wait 2 to 6 months before finding a buyer for your shares. If you need money tomorrow, SCPIs are not the solution. It is capital to let sit.

There are also entry fees of 8% to 12% depending on the SCPI. This is capital lost on day zero. Annual management fees (0.6% to 1.0%) and potentially exit fees continue to eat into your returns. In reality, after deducting all fees and taxes, the net yield can drop to 3.5% to 4.5%, which remains reasonable but less spectacular than announced on investor forums.

SCPIs via Life Insurance: The Best Approach

Here is the trick that changes everything: put your SCPI shares into a life insurance policy rather than directly. Why? Because you keep all the returns, but benefit from the much more favorable taxation of life insurance. After 8 years, you pay almost no taxes. And you keep the option to switch to other investments without triggering immediate taxes. It’s a win-win all around.

Comparison Table: The Three Face-to-Face

| Criterion | Life Insurance (UC) | Stock Market (PEA) | SCPI |

|---|---|---|---|

| Average annual return | 4.5% – 7.5% (stocks) | 7% – 12% (stocks) | 5% – 7% (2026) |

| Volatility | Moderate to high | High | Low to moderate |

| Recommended horizon | 8+ years (for taxation) | 5+ years (PEA) | 10+ years (long term) |

| Entry fees | 0% (online contracts) | 0% | 8% – 12% |

| Annual fees | 0.5% – 1.0% | ~0.15% (ETF) | 0.7% – 1.0% |

| Taxation (after 8 years) | Very favorable | None (PEA 5 years) | 45% (+ social) |

| Liquidity | Excellent | Excellent | Low (2-6 months) |

| Diversification | Total (1300+ options) | Very good (ETF) | Concentrated (real estate) |

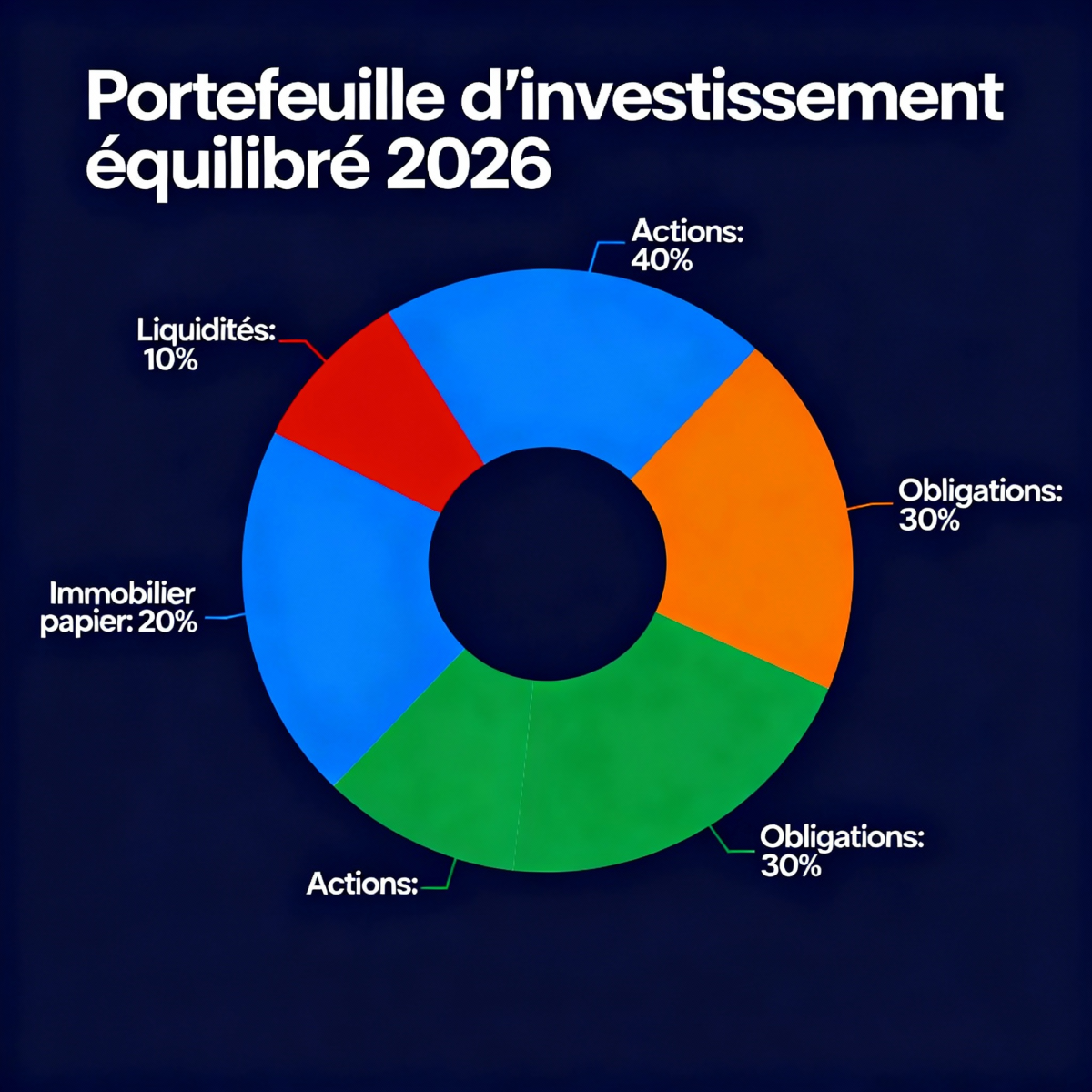

How to Structure Your Portfolio in 2026?

A good strategy does not bet everything on one horse. Wealth diversification is the secret. Here are three typical profiles and their allocations for 2026.

Defensive Profile (Retired or Low Risk Tolerance)

You have few years ahead of you, or simply turbulence stresses you out. Your priority: protect capital and generate regular income.

Suggested allocation:

- 40% life insurance euro funds: reassuring base with guaranteed capital.

- 25% life insurance unit-linked (bonds): stable return, less volatile.

- 20% SCPI via life insurance: regular real estate income.

- 15% cash and savings accounts: emergencies and buying opportunities.

Expected return: 3.5% to 4.5% net annually. Annual volatility: ~5%.

Balanced Profile (Moderate Risk)

You are working, have 10-15 years before retirement, and tolerate moderate fluctuations. This is the profile of the smart investor seeking balance.

Suggested allocation:

- 20% life insurance euro funds: reassuring foundation.

- 30% life insurance equities (diversified ETFs): controlled growth.

- 15% PEA diversified equities: optimal taxation over 5+ years.

- 20% SCPI: rental income.

- 10% bonds or bond funds: additional stability.

- 5% cash: flexibility.

Expected return: 5.5% to 7.0% net annually. Annual volatility: ~12%.

Aggressive Profile (Young or High Tolerance)

You have 20+ years ahead, fluctuations do not worry you. You are ready to take risks to maximize growth.

Suggested allocation:

- 15% life insurance euro funds: minimal reassuring ballast.

- 35% PEA equities / global ETFs: maximum growth, zero taxation.

- 25% life insurance equities and emerging ETFs: global exposure.

- 15% SCPI: real estate diversification.

- 10% private equity or growth funds: maximum potential.

- 5% cash: opportunities.

Expected return: 7.5% to 10.0% net annually. Annual volatility: ~18%.

The 2026 Tax Reforms: What Changes For You

The 2026 Finance Law is not just a dull document. It contains concrete measures that directly impact your investment decisions.

Exemption of real estate capital gains in 17 years

Until now, you had to wait 22 years to be exempt from tax on real estate capital gains, and 30 years for social contributions. A nightmare for investors.

The adopted amendment shortens the period to 17 years for tax exemption, which frees up part of the capital earlier. This is interesting if you plan to sell a rental property in the coming years. Social contributions remain aligned with the 30 years.

Tax depreciation for private landlords

The reform also introduces an annual tax depreciation up to 5% over 20 years for landlord owners. Practically, this means you can deduct a portion of your property’s cost each year for tax purposes. This reduces your taxable income and therefore your tax.

Result? An owner who rents out a property with a good EPC (A or B) can benefit from a tax deduction of more than 50% on their rental income. This makes rental property investment much more attractive in 2026.

Traps to Avoid in 2026

Here are the common mistakes savers make and that must be avoided at all costs.

❌ Leaving everything in the Livret A

The Livret A rate drops to 1.5% in February 2026. That’s a 50% drop in one year compared to current rates. Worse: 1.5% is below inflation. Your money slowly erodes month after month. If you have reached the ceiling of €22,950, moving your funds to a life insurance policy or an SCPI becomes urgent.

❌ Concentrating 100% in unit-linked accounts without a base

Stocks rise and rise quickly, then they plunge. Keeping a base of 20-30% in euro funds or bonds allows you to sleep soundly when the market cools down.

❌ Buying SCPIs without studying their portfolio

Not all SCPIs are equal. Some are concentrated on aging office buildings (bad for 2026-2030). Others are diversified geographically and sectorally. Read the management reports, check the portfolio composition, ask for advice.

❌ Forgetting tax thresholds

If you have had a life insurance policy for less than 8 years, you will pay heavily in taxes if you withdraw. If you hold stocks in a regular securities account, you will pay 36.2% total tax. Respect the horizons and the envelopes.

❌ Reacting to emotional shocks

The stock market plunges in 2026? That’s normal. Staying firm during slowdowns is how real gains are made. Studies show that investors who change strategy during crises lose big.

Verdict: How to Choose in 2026?

Life insurance remains the undisputed champion for mixed profiles. It is flexible, fiscally efficient after 8 years, and you fully control your risk. If you don’t have a contract, open one now even with €500. Entry fees are zero with good providers.

The stock market via PEA is unbeatable for long-term returns and for young investors. The total tax exemption after 5 years is generous. If you are starting your savings, this is your priority.

SCPIs excel for regular and accessible income. But buy them via a life insurance policy rather than directly, unless you are an expert. Entry fees direct are too high.

In 2026, build a balanced portfolio that combines three elements:

- A reassuring base: 40-50% euro funds + bonds.

- A growth engine: 30-40% diversified stocks and ETFs.

- Regular income: 15-25% paper real estate SCPI.

This triple approach allows you to combine security, return, and liquidity. It’s the art of smart investing: it’s never 0 or 100, it’s always a clever mix according to who you are and what you aim for.

FAQ: Questions You Are Asking Yourself

Is it really necessary to open a life insurance policy in 2026 if it’s for 20 years?

Yes, without hesitation. Time is on your side. With 20 years ahead of you, market volatility becomes almost insignificant. And the ultra-favorable taxation after 8 years makes the difference. Even €500 per month invested in a multi-support life insurance policy for 20 years can yield a respectable estate of €150,000 to €200,000.

SCPI or real estate funds (FPI) in life insurance?

Both work. SCPIs offer a higher average return (5-8%) but are illiquid. Listed real estate funds (FPI or real estate companies listed on the stock exchange) offer about 3-5% return but are instantly liquid. For most, a mixed allocation (70% SCPI, 30% listed real estate companies) in life insurance balances return and liquidity.

Will the CAC 40 really rise in 2026?

Technical indicators and the expected drop in ECB rates point to a probable increase. But “probable” is never “certain.” Geopolitical crises and economic shocks can overturn everything. Keep a long-term strategy, not short-term bets on rises.

Should I wait 8 years to withdraw from my life insurance tax-free?

No, you can withdraw whenever you want. But if you withdraw before 8 years, you will pay tax and social contributions. After 8 years, taxation becomes almost nonexistent. So yes, if you have a long horizon, wait for the 8 years. If you might need money, put it in savings accounts rather than unit-linked investments.

How to choose between 10 different SCPIs?

Forget the displayed returns. Instead, look at the portfolio composition (geography, sectors), management quality, 10-year track record, and geographic diversification. The best SCPIs in 2026 are those well-managed for a long time, not the shooting stars of the moment.

What if I need to keep my money liquid for an emergency?

Keep 3 to 6 months of expenses in a Livret A or Livret d’Épargne Populaire (LEP if you are eligible). The rest can go into investments. But don’t lock everything up because you “might” need it. That’s the classic trap that keeps you permanently underperforming.

Are bonds attractive in 2026?

Yes, more than before. French government bond yields hover around 3.5-4.5%, which is acceptable. Corporate bonds (BBB) target 4.5-5.5%. That’s decent as a complement to an equity allocation. A 60% equity / 40% bond allocation remains classic and robust.

What is the best time to invest in 2026?

Now. Or yesterday. Market timing doesn’t exist. What works is regular investing. Deposit €100 or €500 each month, no matter if it’s high or low. Over time, the highs and lows even out and you profit. This is called dollar-cost averaging, and it’s your best friend.

Conclusion: Be Boring, Be Rich

2026 won’t be revolutionary, but it will mainly be a year of consolidation. ECB rates will probably remain stable around 2%. Stock markets should progress but not explode. Real estate yields will normalize. This means those who diversify now, accept long horizons, and respect tax wrappers will quietly win, without stress.

Here’s the real recipe in 2026: be boring, disciplined, and patient. Open a multi-support life insurance policy. Contribute regularly. Mix euro funds, stocks, bonds, and SCPIs. Let the 8 years pass. Then reap the benefits of ultra-favorable taxation. It’s not sexy, but it’s profitable. And that’s how real wealth is built in France.